Best Business Credit Cards for Small Entrepreneurs in the U.S.

Small business owners in the United States often face a common challenge: managing cash flow while accessing the capital they need to grow. One of the most powerful tools at their disposal is the business credit card—a flexible financial instrument that, when chosen wisely, can unlock rewards, build credit, and streamline expenses. But with hundreds of cards on the market, how do you determine which ones truly align with your business goals?

Why Business Credit Cards Matter for Small Entrepreneurs

1. Building Business Credit History

Establishing a strong business credit profile is essential for securing future financing. Business credit cards report to commercial credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business. Regular usage and timely payments improve your credit standing, which can lower your interest rates on loans and increase your financing options down the road.

2. Managing Cash Flow & Operational Expenses

With billing cycles and grace periods, business credit cards provide short-term access to capital. Entrepreneurs can purchase inventory, cover marketing expenses, or pay for software tools even when immediate cash isn’t available. This flexibility allows smoother operation and peace of mind during revenue dips.

3. Earning Rewards Tailored to Business Needs

Business credit cards offer cashback, travel miles, or points that can be reinvested into the business. Choosing a card aligned with your highest spending category—be it gas, office supplies, or digital advertising—maximizes the value of every dollar you spend.

4. Simplifying Bookkeeping and Tax Reporting

Detailed expense tracking through monthly statements, categorized purchases, and integration with accounting software like QuickBooks helps entrepreneurs manage finances efficiently and prepare for tax season.

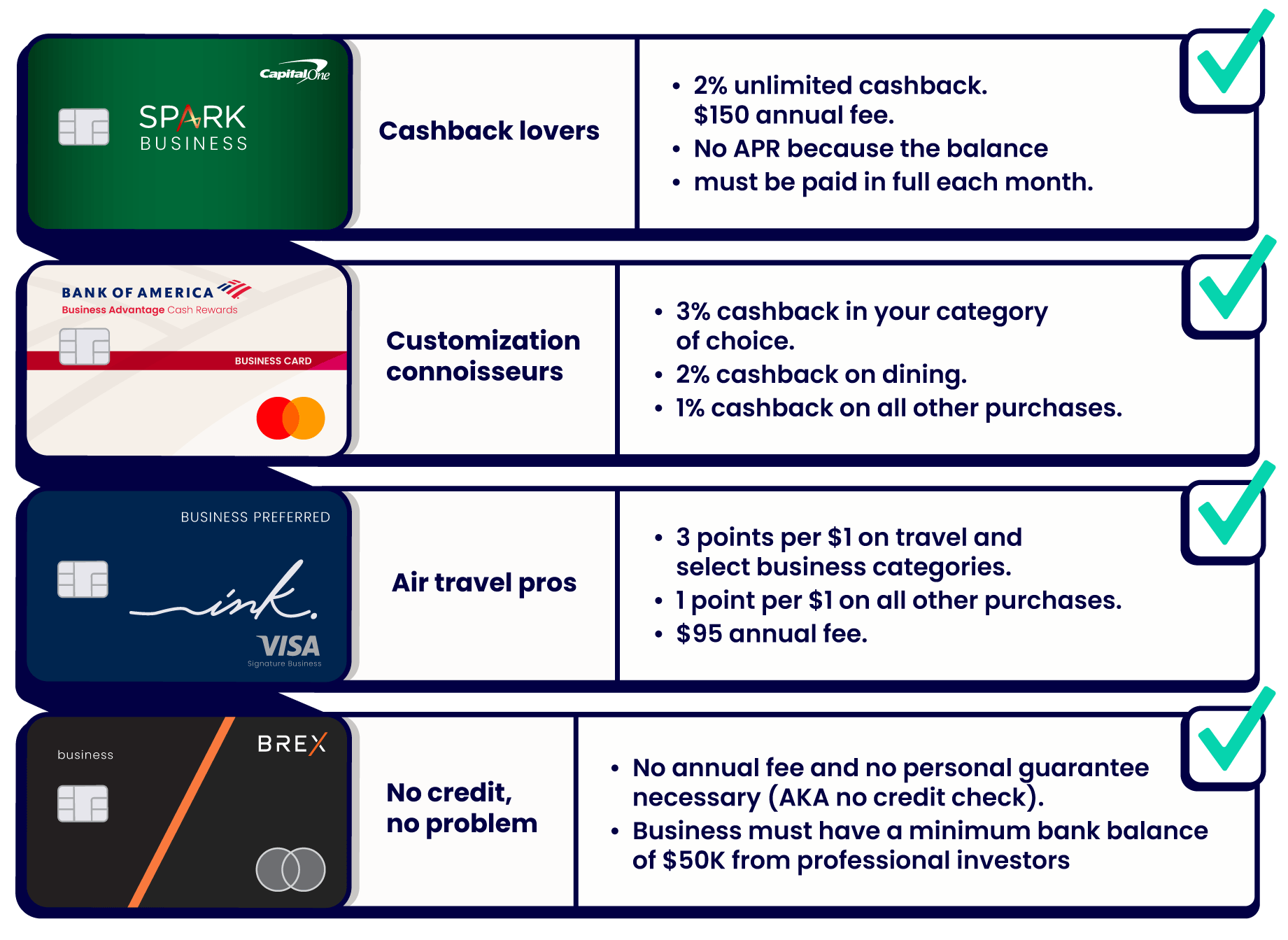

Top Business Credit Cards for Small Entrepreneurs in 2025

| Card | Annual Fee | Rewards | Intro APR | Best For |

|---|---|---|---|---|

| American Express Blue Business Plus | $0 | 2X points on all eligible business purchases (up to $50K/year) | 0% for 12 months | Flat-rate rewards seekers |

| Chase Ink Business Cash | $0 | 5% on office supplies & internet; 2% on dining & gas | 0% for 12 months | Category spend maximizers |

| Capital One Spark Cash Plus | $150 | 2% unlimited cash back | N/A (charge card) | High spenders |

| Brex Card for Startups | $0 | Up to 7x points on select categories | Net 30 days | Tech & venture-backed startups |

Real-World Use Cases: Matching Cards to Business Needs

Scenario 1: A Freelance Graphic Designer

Profile: Monthly expenses include software subscriptions, advertising, and occasional hardware purchases. Prefers digital payments and travels occasionally for conferences.

Recommended Card: American Express Blue Business Plus. The flat 2X points ensure that no dollar goes unrewarded regardless of category.

Scenario 2: A Small E-Commerce Retailer

Profile: Regular spending on shipping, online ads, inventory, and web tools. Wants robust reporting and budget management.

Recommended Card: Chase Ink Business Cash. The 5% cash back on internet and office supply services helps reduce core operating costs.

Scenario 3: A Growing SaaS Startup

Profile: Backed by investors, rapid hiring, high digital ad spend, and wants flexible scaling tools.

Recommended Card: Brex Card for Startups. No personal guarantee required, tailored rewards, and integration with platforms like Slack and Xero.

Key Considerations When Choosing a Business Credit Card

1. Personal Liability vs. Business Liability

Many business cards require a personal guarantee, making you personally responsible for repayment. Some fintech cards like Brex offer options without personal liability, but require robust business finances or venture backing.

2. Expense Categories & Reward Alignment

Analyze where your business spends the most and align your credit card rewards accordingly. Use aggregated data from bookkeeping tools or review past statements.

3. Welcome Bonuses

Cards like Chase Ink Business Preferred offer up to $1,000 in value through introductory bonuses. But ensure your spend volume realistically matches the requirements.

4. Annual Fees and Hidden Charges

Don’t be discouraged by higher annual fees if the rewards far outweigh them. But always review terms regarding foreign transaction fees, late payment penalties, and APRs.

Credible Sources and Expert Perspectives

- Forbes Advisor: Identifies the Chase Ink Business suite as a leading choice in 2025 for flexible cashback structures. (Source)

- NerdWallet: Rates AmEx Blue Business Plus as “best for everyday expenses” due to its simple, generous reward model.

- U.S. Small Business Administration (SBA): Emphasizes building credit through consistent use of business credit cards.

“The best business credit card is one that grows with your company. From cashback to scalable rewards, it should reflect your evolving needs.” — Jordan Tarver, Forbes Finance Editor

Tips for Maximizing the Value of Your Business Credit Card

- Set category-specific cards for different departments (e.g., ad spend vs. logistics).

- Use expense management tools like Ramp, Divvy, or QuickBooks to integrate and monitor transactions in real time.

- Pay in full each month to avoid high APR interest fees.

- Assign virtual cards to employees with preset limits for better control.

- Redeem points strategically for travel, gift cards, or statement credits to reinvest into the business.

Common Pitfalls to Avoid

- Mixing Personal and Business Expenses: Blurs financial records, reduces tax efficiency, and can hurt business credit scores.

- Missing Payments: Damages credit history and may result in penalty APRs or revoked rewards.

- Choosing a Card Based Only on Bonus Offers: Intro bonuses are attractive, but long-term value depends on reward structure and business fit.

Conclusion: Choosing the Right Business Credit Card Pays Off

Business credit cards are more than just a payment method—they are strategic financial tools. When selected with your business model, cash flow, and goals in mind, they provide tangible value through rewards, credit building, and expense management. Whether you’re a solo entrepreneur or managing a team of 50, aligning your spending with the right card unlocks compounding benefits.

Key Takeaways:

- Choose cards based on where your business spends most.

- Look for long-term reward structures—not just flashy intro offers.

- Use business cards to build credit and track expenses efficiently.

Ready to Elevate Your Business Finances?

At insurance.basicsuri.com, we help entrepreneurs make smarter financial decisions—from comparing insurance plans to optimizing your credit strategy. Start today by exploring our tailored tools and automated insights built just for small businesses.

Don’t wait—choose the right business credit card and fuel your business growth in 2025.